Planning for retirement in Iowa encompasses various financial aspects, from accumulating savings to managing investments, and envisioning your desired lifestyle. While many focus on building a robust nest egg, overlooking the potential need for long-term care can jeopardize financial security in later years.

In today’s economic environment, incorporating long-term care insurance into your retirement plan isn’t merely an option; it’s becoming a necessity.

Let’s delve into the importance of long-term care insurance and why it should be an integral component of your retirement strategy.

The Rising Need for Long-Term Care

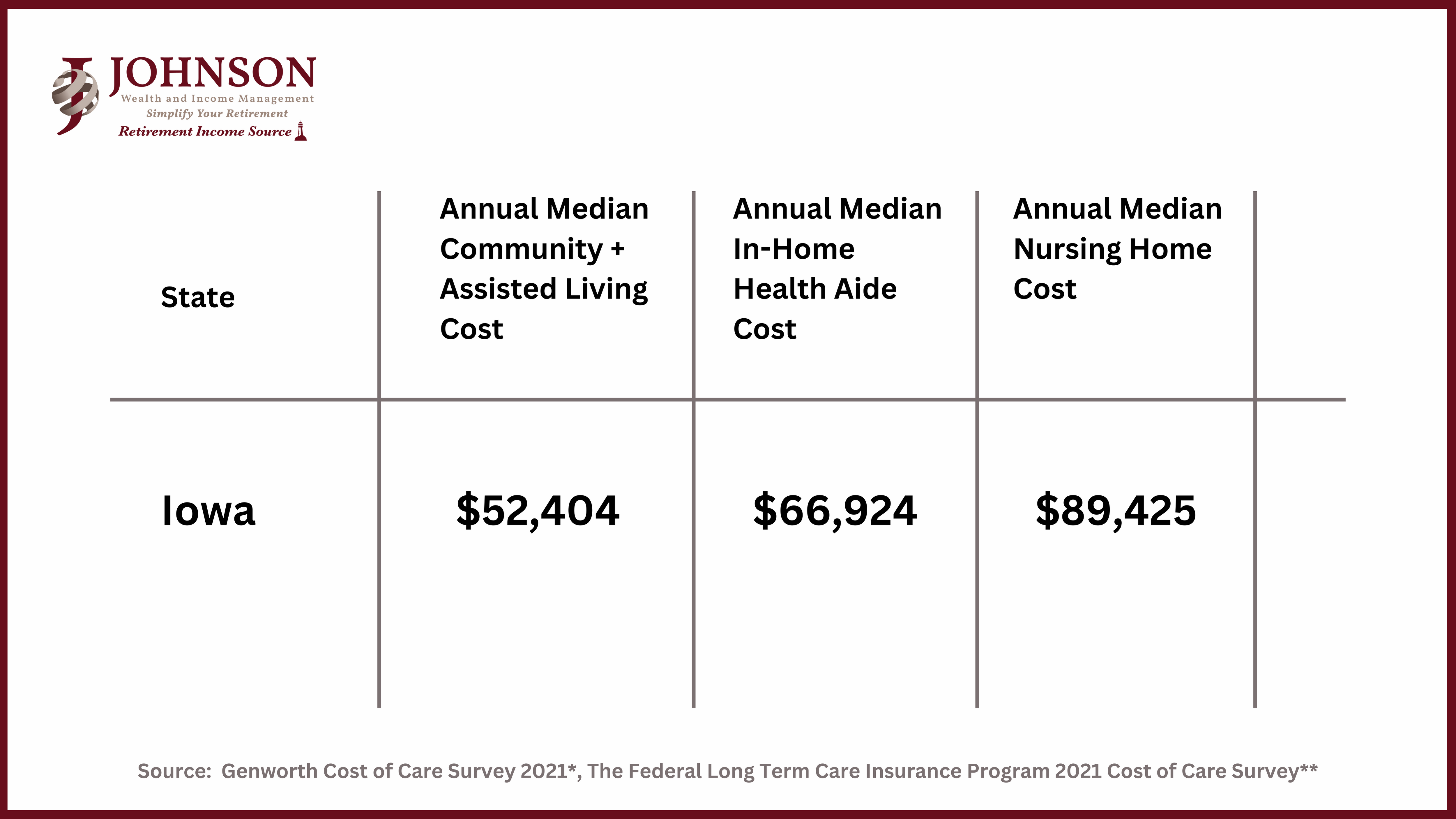

As life expectancies increase, so does the likelihood of requiring long-term care services due to age-related illnesses, chronic conditions, or unforeseen health events. In fact, 70% of adults aged 65 years and older will require long-term care at some point in their life, this could range from assistance with daily activities to specialized medical services. One-third of people may never need long-term care, but 20% will need it for longer than 5 years. On average women need 3.7 years of care while men need 2.2 years. In 2022, the average cost for 3 years of long-term care in Iowa was $268,275 ($89,425 per year). That cost is projected to be $484,533 ($161,511 per year) in 2042.

Without adequate coverage, the exorbitant costs associated with long-term care can deplete your retirement savings, undermining financial independence, and possibly even burdening loved ones. Take a look at the average cost of long-term care in Iowa.

Help Protect Retirement Assets

Integrating long-term care insurance into your retirement plan helps safeguard against the potentially devastating financial implications of extended care needs. By securing a comprehensive long-term care policy, you create a dedicated fund to cover expenses related to nursing homes, assisted living facilities, in-home care, and other essential services. This proactive approach helps preserve your retirement assets, helping ensure you can maintain your desired quality of life without exhausting your savings or compromising your legacy goals.

It’s a good idea to consider getting long-term care insurance in your fifties or early sixties. Here’s why:

- If you buy a policy when you’re younger, your yearly payments will be lower.

- Even though you’ll be making payments for a longer time, the total cost will usually be less compared to buying it when you’re older.

- Waiting until your mid-sixties might lead to health issues that could make it harder to get insurance or qualify for discounts.

So, waiting usually doesn’t make sense. Plus, you won’t have coverage while you wait, and if you have an accident or illness, you’ll have to pay for long-term care on your own.

Working with a Fiduciary advisor can add a layer of protection, as they can help you assess the appropriate coverage levels based on your financial situation. They can also assist in coordinating your long-term care insurance with other retirement income sources and investment portfolios, help optimize cash flow, tax efficiency, and asset allocation strategies. By integrating long-term care planning within a holistic retirement framework, your financial advisor helps fortify your assets, mitigate risks, and navigate complex healthcare decisions with confidence and foresight.

Managing Health and Lifestyle Choices

Beyond financial considerations, long-term care insurance empowers you to make informed health and lifestyle choices aligned with your preferences and values. Having coverage provides peace of mind, knowing you have access to quality care options and resources when needed. Whether opting for in-home assistance, specialized medical treatments, or residential care facilities, long-term care insurance grants you flexibility and helps you gain control over your care decisions, helping to foster independence and dignity in your later years.

Tax Advantages and Policy Customization

Long-term care insurance also offers a potential tax advantage and policy customization options can be tailored to your unique needs and circumstances. Depending on the policy features and structure, you may benefit from tax-qualified premiums and favorable tax treatment on benefits received.

Certain conditions can render benefits received from a qualified long-term care policy tax-free, offering additional financial relief during critical periods. A knowledgeable Fiduciary advisor can help guide you through these complexities, helping you maximize tax benefits while aligning your coverage with your unique needs, risk tolerance, and retirement objectives.

How Johnson Wealth and Income Management Can Help

At Johnson Wealth and Income Management, we prioritize your financial well-being by offering tailored retirement planning solutions that encompass comprehensive strategies, including long-term care insurance integration. Our seasoned team of advisors collaborate closely with you to understand your unique retirement goals, risk tolerance, and healthcare needs; crafting a personalized roadmap that aligns with your aspirations.

By leveraging our expertise (knowledge) and industry insights, we’ll guide you through the complexities of long-term care insurance, evaluating policy options, tax implications, and coverage levels to safeguard your assets and lifestyle in later years. With Johnson Wealth and Income Management by your side, you gain peace of mind, knowing you have a robust retirement plan supported by meticulous planning, proactive advice, and unwavering commitment to your financial success and well-being.

Final Thoughts

Integrating long-term care insurance into your retirement plan is a prudent and essential step toward helping secure financial stability, it can also help protect assets and maintain autonomy in your later years. Acknowledging the potential need for long-term care and proactively addressing it through comprehensive insurance coverage can help mitigate risks, alleviate financial strain, and enhance your overall retirement readiness.

Consult with financial professionals to explore long-term care options, evaluate policy features, and develop a holistic retirement strategy that prioritizes your long-term well-being and peace of mind.